NEW ESTATE TAX AMNESTY AND QUARANTINE BIR REGULATIONS

By Euney Marie Mata-Perez on August 12, 2021

To the relief of many taxpayers, Republic Act (RA) 11569 was passed amending RA 11213 (Tax Amnesty Act) and extending the availment of the tax amnesty to June 14, 2023.

In accordance thereto, the Bureau of Internal Revenue (BIR) issued Revenue Regulations (RR) 17-2021, which amends the previous regulation RR 6-2019 and implements the extension of the estate tax amnesty. Like the previous regulation, RR 17-2021 still requires the filing of estate tax amnesty return (ETAR), acceptance payment form and the supporting documents.

RR 17-2021 further provides that the proof of settlement of estate, whether judicial or extra-judicial, need not accompany the ETAR, if such proof of settlement is still not available at the time of filing. However, the electronic certificate authorizing registration (eCAR) shall not be issued unless the proof of settlement is presented and submitted to the revenue district officer concerned. This is good news for the families and heirs who intend to avail the amnesty, but are unable proceed because of their inability to agree on the settlement of estate or division of properties.

RR 17-2021 provides though that, if the proof of settlement of estate (i.e., extra-judicial agreement in case of extra-judicial settlement of the estate or court order in case of judicial settlement) enumerates properties not indicated in the ETAR, such excluded properties shall not be included in the eCAR, unless additional estate tax amnesty payment shall be made for them. The submission, however, has still to be made within the amnesty period. Otherwise, such additional properties shall be subject to the regular estate tax rates applicable at the date of death of decedent, plus interests and penalties.

On Aug. 10, 2021, the BIR issued Revenue Memorandum Circular (RMC) 94-2021, which addresses situations where heirs, in their settlement of the estate, do not get equal shares or values of the properties inherited. While a general renunciation of an inheritance is not subject to any donor’s tax, the 6-percent donor’s tax will be due when some heirs get more than shares or values over the others.

These new issuances make it now easier to avail of the estate tax amnesty. Thus, heirs and families should exert effort to avail of the amnesty within the new extended period.

ECQ/MECQ regulations

The BIR has also issued the following issuances in light of the new quarantine restrictions imposed in the National Capital Region and other areas:

RMC 91-2021 (Aug. 3, 2021) – Provides the guidelines in the filing of returns and payment of the corresponding taxes due thereon, and submission of reports and attachments falling within the period from Aug. 6 to 20, 2021 for taxpayers under enhanced community quarantine (ECQ) and modified enhanced community quarantine (MECQ). The deadline for filing of returns and payment of the corresponding taxes falling within the abovementioned dates are extended for a period of 15 calendar days from Aug. 20, 2021. However, if the ECQ and/or MECQ will be extended, then filing and payment of the corresponding taxes due thereon, and submission of reports and attachments falling within the period shall also be extended by 15 calendar days from the lifting of the ECQ and/or MECQ.

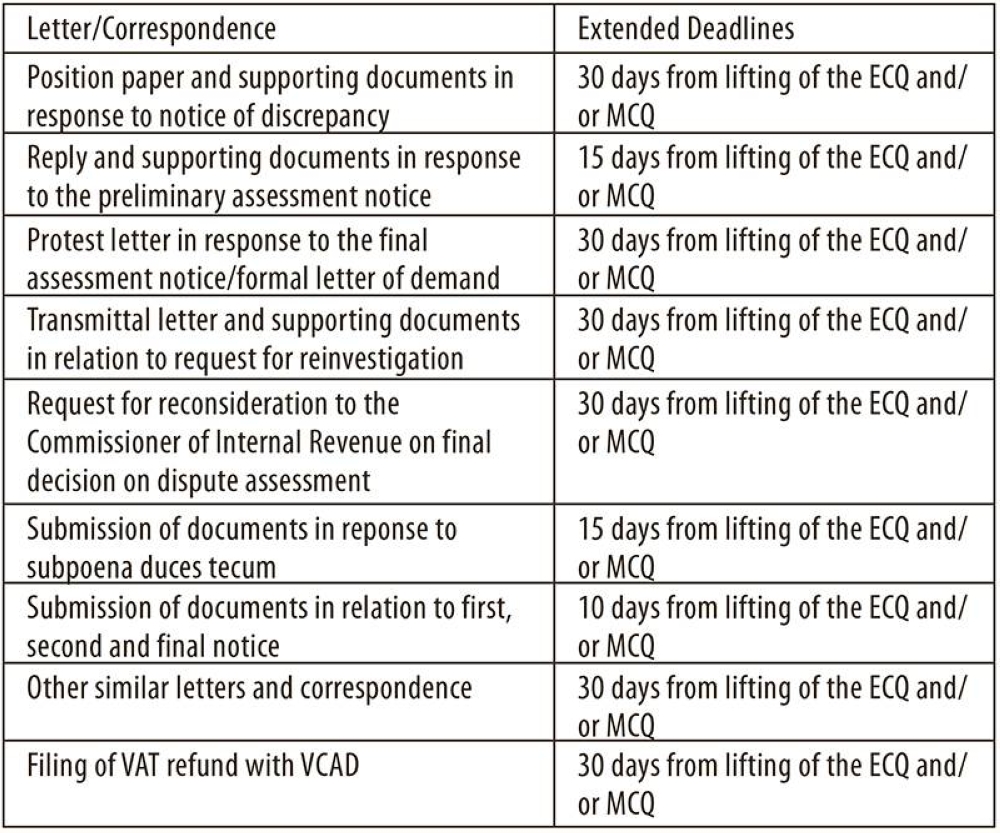

RMC 92-2021 (Aug. 9, 2021) – Extends the deadline for filing of position papers, replies, protests, documents and other similar letters and correspondences in relation to the ongoing BIR audit investigation, and filing of claim for refund of value-added tax (VAT) with the VAT Credit Audit Division (VCAD) due to the declaration of ECQ and MECQ in the National Capital Region and other areas of the country, as follows: (See table above)

RMC 93-2021(Aug. 9, 2021) – Provides that the running of the statute of limitations on assessment and collection of taxes pursuant to Section 223 of the Tax Code 1997, as amended, is suspended in the affected jurisdictions while ECQ and/or MECQ is in effect, including any extension/s thereof, and for 60 days thereafter. The suspension of the running of the statute of limitations shall apply with respect to the issuance and service of assessment notices, warrants and enforcement, and/or collection of deficiency taxes.

Taxpayers should thus be mindful of these new extended deadlines.

#RA11213 #AmendedTaxAmnestyAct #EstateTaxAmnesty #TaxAmnestyExtension #QuarantineRegulations

Euney Marie J. Mata-Perez is a CPA-Lawyer and the managing partner of Mata-Perez, Tamayo & Francisco (MTF Counsel). She is a corporate, M&A and tax lawyer and has been ranked as one of the top 100 lawyers of the Philippines by Asia Business Law Journal. This article is for general information only and is not a substitute for professional advice where the facts and circumstances warrant. If you have any question or comment regarding this article, you may email the author at info@mtfcounsel.com or visit MTF website at www.mtfcounsel.com.